Client: Licensed Moneylender Singapore | Synergy Credit

Written By: The Big Writer

Published At: Read More

Key Takeaways

- Being unable to pay a money lender in Singapore does not automatically lead to jail or immediate court action, but it should still be addressed early to avoid escalation.

- Licensed money lender late payment charges are regulated in Singapore, with capped late fees and interest to prevent the accumulation of excessive debt.

- If you are unable to pay your money lender, communicating early with your lender can open the door to a money lender debt repayment plan tailored to your unique situation.

- Licensed money lenders may take legal action if repayments are not resolved, so knowing the answer to the question “Can a money lender file a case in court?” is important for borrowers.

- Turning to an “ah long” money lender or ignoring the issue can complicate matters, whereas exploring solutions such as a debt consolidation loan in Singapore or a personal loan for debt consolidation may help you manage multiple debts more effectively.

Finding yourself unable to make a loan repayment can be stressful, especially when bills are already piling up. If you are unable to pay your money lender in Singapore on time, you may be worried about late fees, legal action, or how the situation could affect your financial future. While missing a payment should not be taken lightly, it is important to know that all is not lost—there are practical steps you can take to address the problem.

Rather than avoiding your licensed money lender or seeking quick cash from an “ah long” money lender, understanding your rights and responsibilities can help you make informed decisions. The sooner you communicate with your licensed money lender, the more options you may have to manage the situation responsibly.

What Happens if You Are Unable to Pay a Money Lender?

Being unable to pay your money lender instalments on time can lead to several consequences, but knowing what to expect can help reduce uncertainty in this nerve-wracking situation.

#1 The Lender May Contact You About the Missed Payment

When a repayment is missed, a licensed money lender will typically reach out via phone calls, text messages, emails, or written notices. These communications are intended to remind borrowers of their outstanding obligations and discuss possible next steps.

While lenders may contact borrowers about overdue payments, they must do so lawfully. Harassment, threats, public shaming, intimidation, and other abusive practices are not acceptable methods of debt recovery and should never be tolerated.

#2 Late Fees and Late Interest May Apply

In the event that late payment to a licensed money lender is inevitable, you may be liable for additional charges. However, know that these are strictly regulated:

- Late Fee: Capped at S$60 per month for each overdue repayment, regardless of the total number of missed instalments

- Late Interest: Capped at 4% per month on the overdue amount only

- Total borrowing costs (including interest and fees): Must not exceed 100% of the original principal loan amount

#3 Future Borrowing May Be Impacted

Late or missed payments may affect your future loan applications. Licensed money lenders report loan information to the Moneylenders Credit Bureau (MLCB), which maintains records of borrowers’ loan obligations and repayment records in the licensed moneylending sector.

As part of the application process, all licensed lenders must review this information before determining your loan eligibility. Consistently meeting repayment obligations can strengthen your borrowing profile, while repeated late payments may reduce your creditworthiness and make it more difficult to obtain financing in the future.

Can You Go to Jail for Not Paying a Licensed Money Lender?

No, you will not go to jail for not paying a licensed money lender in Singapore. Unpaid debt is typically treated as a civil matter and not a criminal matter, meaning you cannot be imprisoned solely for being unable to repay. However, they may take legal action through the civil courts to recover the debt owed if repayment discussions fail—this is why it’s important to communicate early rather than ignore the situation.

That said, cases involving fraud are different. Providing false information, forged documents, or deliberately misleading details during a loan application may lead to criminal consequences, which can carry more serious penalties.

Can a Money Lender File a Case in Court in Singapore?

A common question that many borrowers have is this: “Can a money lender file a case in court?” The answer is yes—if a borrower defaults on a loan and an alternative repayment arrangement cannot be negotiated, a licensed money lender may commence legal proceedings to recover the outstanding debt.

Court action is generally a last resort by lenders after all means to resolve the matter have been exhausted.

What Court Action May Mean for Borrowers

If the civil court rules in favour of the lender, the borrower may be required to pay the outstanding loan balance, plus any applicable interest, fees, and court-ordered legal costs.

It’s important to bear in mind that every case is different, and outcomes depend on the specific facts and circumstances involved.

Court Action Is Different From Harassment

Borrowers should understand that lawful debt recovery is not the same as harassment—legitimate recovery actions must follow strict legal boundaries. A licensed lender cannot threaten violence, damage property, use abusive language, or publicly shame borrowers.

What You Should Do if You Cannot Repay on Time

If you find yourself in situations where you are unable to pay a money lender, taking early action is important:

- Review your loan agreement to double-check the repayment terms and late fee conditions

- Contact your lender as soon as possible before the situation escalates

- Negotiate a manageable money lender debt repayment plan to adjust your repayment schedule or lower your monthly instalments

- Consider longer term solutions, such as getting a debt consolidation loan in Singapore, especially if you have multiple debts

What You Should Not Do When You Are Unable to Pay a Money Lender

If you are unable to pay a money lender, avoiding costly missteps is just as important as taking the right actions early:

- Do not ignore calls, messages, or repayment notices from your lender

- Do not turn to an “ah long” money lender, as you are likely to be exposed to risks of illegal and unsafe recovery methods

- Do not agree to unclear rollover arrangements that may increase your total debt without fully understanding the implications e.g. having to pay more in total

- Do not take on a new loan to pay off your existing loan (unless it’s a debt consolidation loan), as this can result in a vicious cycle of debt

- Do not delay seeking help due to embarrassment, as early communication often leads to better outcomes

What if a Money Lender Harasses or Threatens You?

Know What Is Not Allowed

Licensed money lenders must follow legal debt recovery practices. Harassment, intimidation, threats, abusive language, public shaming, and property damage are unlawful and must not be tolerated.

Keep All Evidence

If you believe you’re on the receiving end of inappropriate conduct, retain any evidence that support your complaint. This may include messages, call records, photographs, videos, letters, and details of any witnesses.

Report Serious Threats Immediately

If there is an immediate threat to your safety, contact the police without delay. Complaints involving misconduct by licensed money lenders may also be reported to the Registry of Moneylenders for investigation.

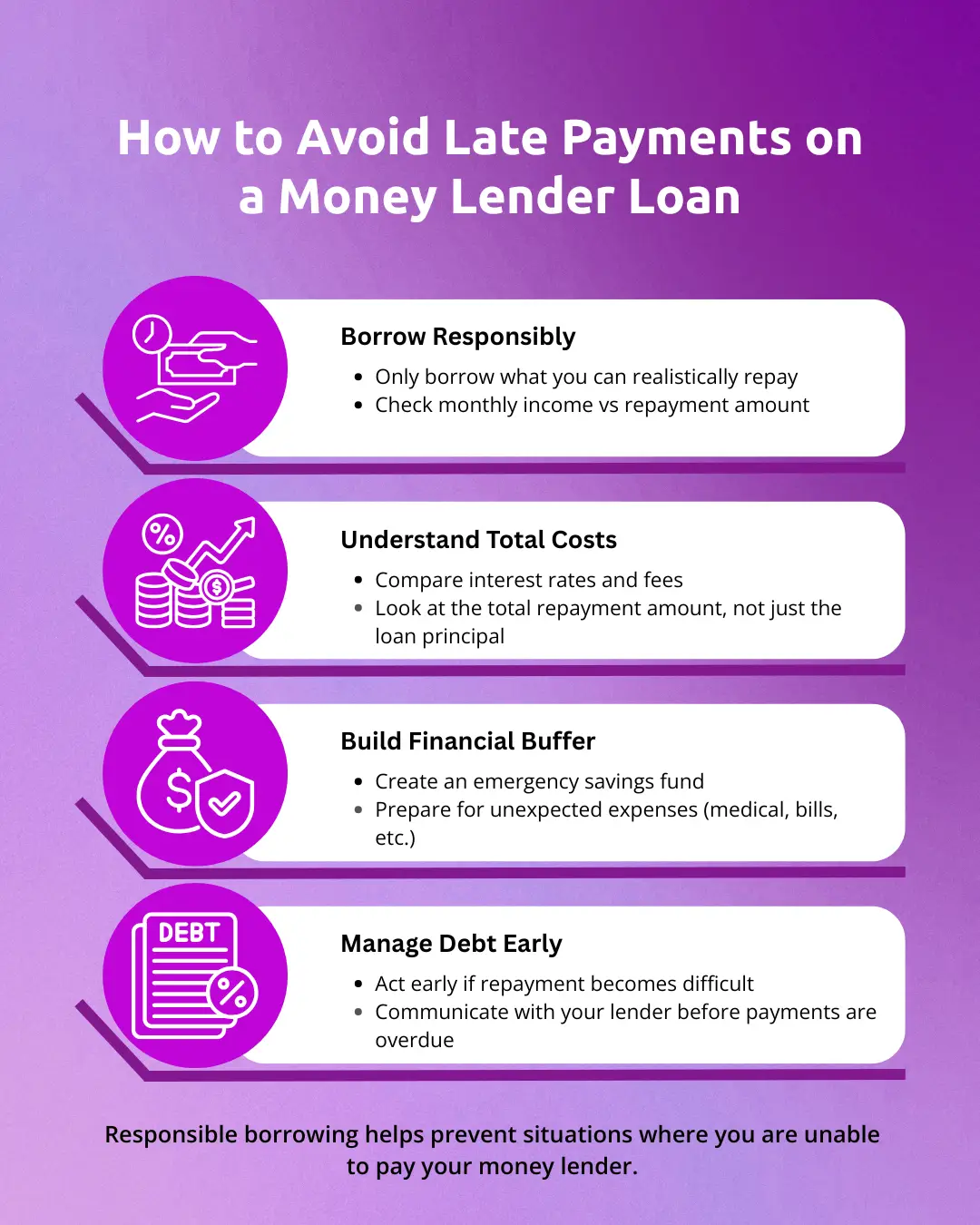

How to Prevent Late Payment Problems in Future

Managing debt successfully often begins with the financial choices you make daily:

Final Thoughts

Being unable to pay a money lender in Singapore can feel overwhelming, but ignoring the issue often makes resolution even more challenging. Understanding your rights, communicating with your lender early, and exploring available solutions can help you regain control of your finances and reduce unnecessary stress.

If you are experiencing repayment difficulties, it is often better to seek guidance sooner rather than later. At Synergy Credit, we encourage responsible borrowing and open communication. Our team can help you understand your loan obligations, discuss available repayment options, such as a debt consolidation loan, and provide transparent information to support your financial decision-making.

Contact Synergy Credit today to learn more about how you can secure a loan within your means and your available options.

Frequently Asked Questions

How many payments can you miss before a money lender takes legal action?

There is no fixed number. Lenders typically consider factors such as the amount owed, the borrower’s repayment history, and responsiveness when discussing repayment options.

Can a licensed money lender visit my home?

Licensed money lenders may contact borrowers through lawful channels regarding overdue payments. However, any form of harassment or intimidation is prohibited.

Can I negotiate a money lender debt repayment plan after missing a payment?

In many cases, borrowers can discuss repayment options with their lender. The sooner communication begins, the greater the likelihood of finding a feasible solution that works for both parties.

Will a late payment affect future loan applications?

Potentially, yes. Lenders review your borrowing and repayment history when assessing new loan applications.

Can a money lender charge unlimited late fees?

Absolutely not! Licensed money lenders in Singapore must comply with regulatory limits on late fees, interest charges, and total borrowing costs.

The post Unable to Pay Money Lender in Singapore? Don’t Panic Yet appeared first on Licensed Moneylender Singapore | Synergy Credit.